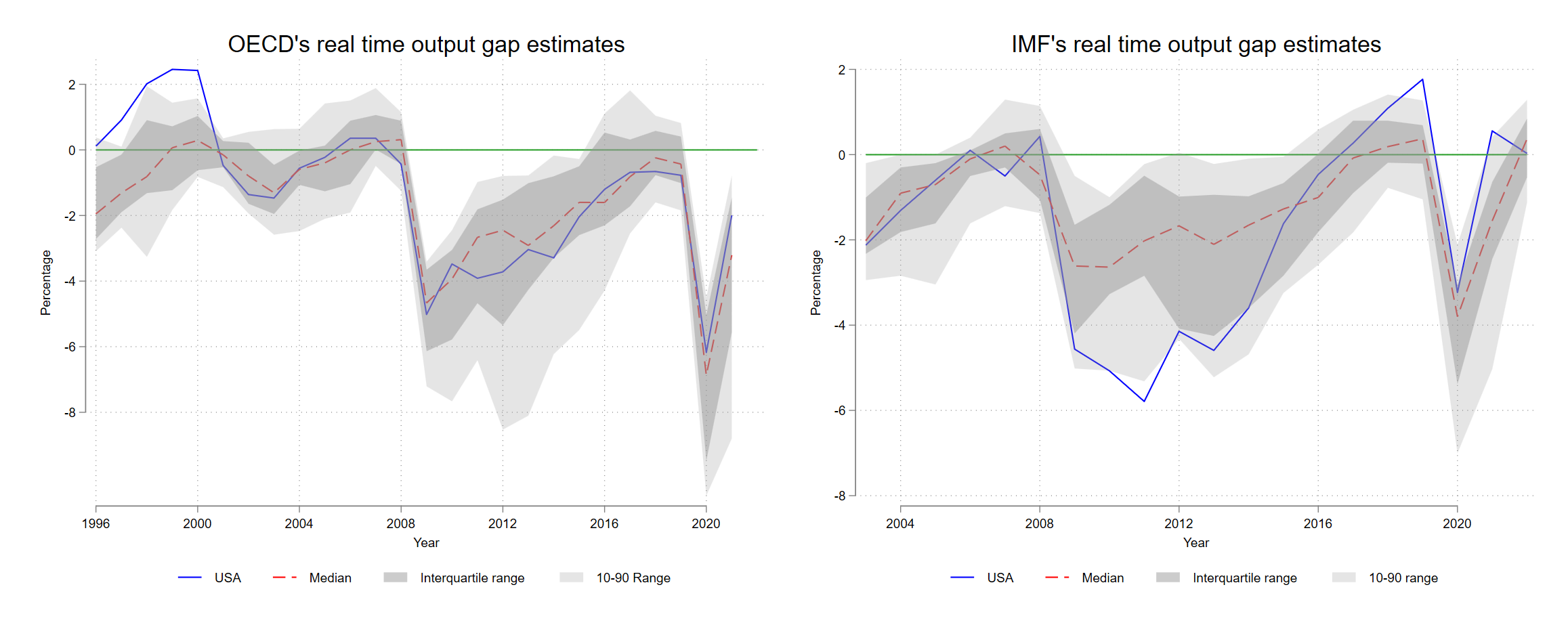

Is there hysteresis in potential output estimates?

Economics Letters · 2024

Abstract

Using an error correction model, this paper studies the dynamics of GDP and potential GDP using OECD's Economic Outlook and IMF's World Economic Outlook estimates of the output gap. The findings suggest the presence of hysteresis, implying that short-run shocks to GDP have sizeable permanent effects on potential GDP.

Keywords

HysteresisPotential GDPerror correction modelBusiness cycleReal time estimates

Highlights

I found hysteresis effects on potential GDP estimates from IMF and OECD.

A 1-unit demand shock has a long-run effect on GDP of about 0.9 percentage points.

The hysteresis elasticity is around 0.28, which is sizeable.

These hysteresis effects are higher on OECD's than IMF's estimates.

The results can be interpreted as a failure of the natural rate hypothesis.

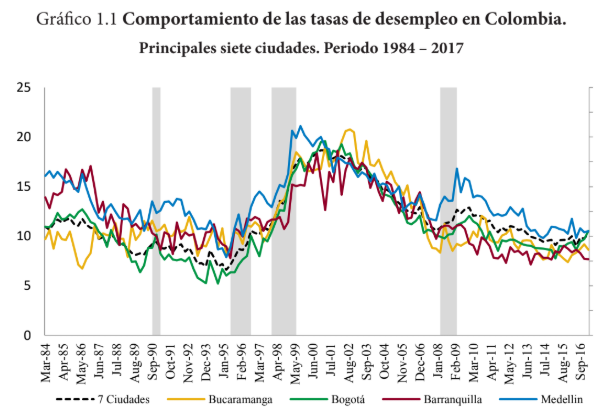

Hysterical but Convergent: The behavior of Colombia's Unemployment Rates

With Karen Lorena Pulido in Colombia. Algunos problemas de hoy visto por los jóvenes · 2021

Abstract

The main objective of the paper is to study the behavior of the unemployment rates in Colombia, during the period between 1984 and 2017. First, we study if unemployment rates are hysterical by using unit root tests. Main results show that unemployment rates are not stationary which rejects the natural rate of unemployment hypothesis. Second, we ask whether changes in cities unemployment differences in Colombia are persistent over time and we found evidence of stochastic convergence in cities unemployment differences. Third, we found stable long-term equilibrium differences in cities unemployment rates.

Keywords

Unemployment rateHysteresisTime seriesBeta convergenceUnit root test

Highlights

Unemployment rates in Colombia's seven major cities exhibit hysteresis.

Despite hysteresis, there is stochastic convergence among most cities' unemployment rates.

Cali, Manizales, Medellín, and Pasto show conditional (not absolute) convergence.

Cities take on average about two years to halve an unemployment shock differential.

The hysteresis finding challenges the use of a constant NAIRU for macroeconomic policy in Colombia.

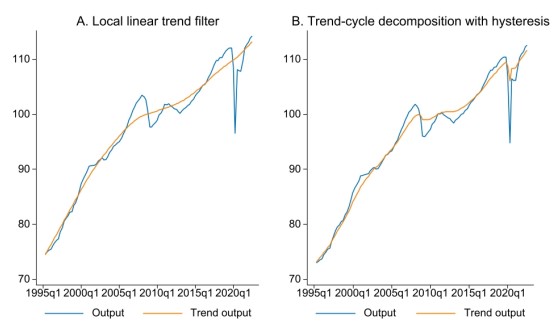

With Javier Gómez-Pineda · Borradores de Economía · 2023

Abstract

The business cycle is the cycle in the output gap and also in a stationary measure of trend output. Both the output gap and trend output are driven by joint trend-cycle shocks. The model is a univariate trend-cycle decomposition with hysteresis in trend output that enables the estimation of the output gap and trend output in 81 economies in quarterly frequency, since 1995Q1; and 184 economies in yearly frequency, in several cases since 1950, and in a few cases since 1820. Volatility and dispersion, as well as the frequency of large joint trend-cycle shocks, were low during the Gilded Age period; high during the interwar period, even more so in advanced (AD) economies compared to emerging market and developing economies (EMDE); and low in AD economies and high in EMDE economies in the post WWII period. In contrast with other existing estimates of trend output, those from the trend-cycle decomposition with hysteresis do not evolve smoothly, do not result in an artificial boom before recessions and are less sensitive to new data.

Keywords

trend-cycle decompositionhysteresisoutput gaptrend outputbusiness cyclelong-run data

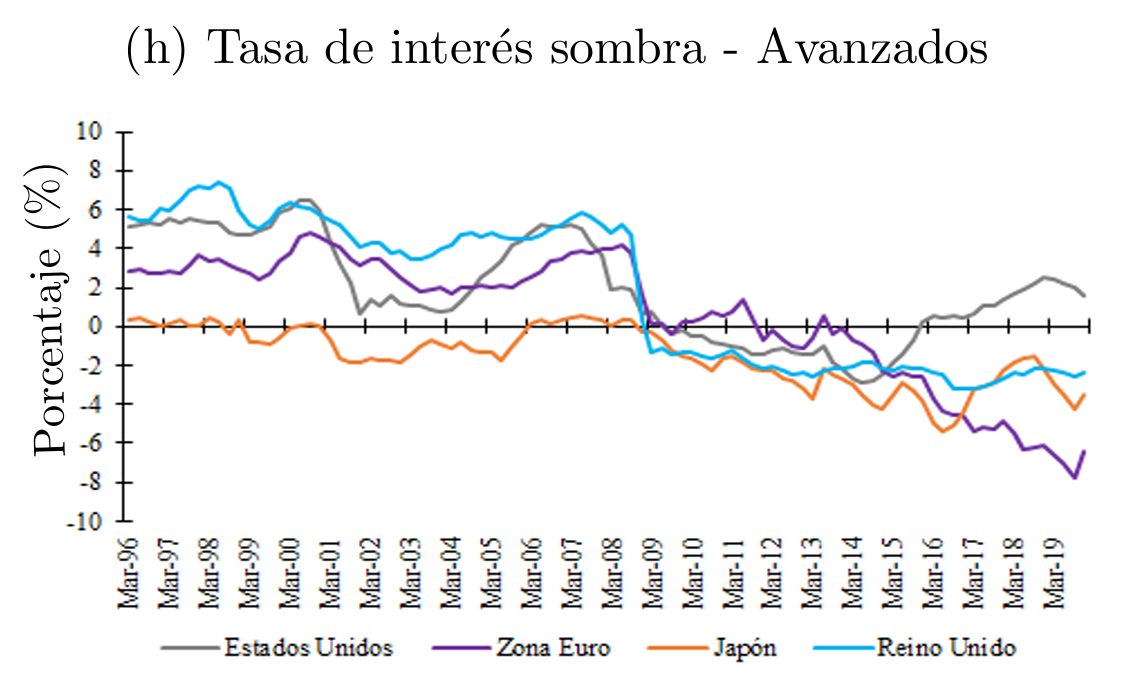

Spillovers of unconventional monetary policy from advanced economies to Latin America

Master thesis published as Documento CEDE · 2021

Abstract

In this paper, I estimate the effects of unconventional monetary policies from the United States, Euro Area, United Kingdom, and Japan (advanced economies) on Mexico, Brazil, Colombia, Chile, and Peru using a global projection model with shadow rates. I find that spillovers are small and the most relevant come from the United States. I also find that volatility spillovers from advanced economies' unconventional monetary policies are negligible. Historical decomposition exercises show that the most affected variables by spillovers are the real exchange rate and inflation. Finally, I simulate counterfactual scenarios in which there were no unconventional monetary policies from advanced economies past 2008, and I find that Latin American economies would have had GDP losses close to 0.5% and inflation 1.5% lower at the end of 2014. This shows the high costs of not implementing these policies — a result that is relevant to the COVID-19 crisis.

Spillovers from advanced economies' unconventional monetary policy to Latin America are small, and the most relevant ones come from the United States.

Volatility spillovers from advanced economies' UMP to Latin America are negligible.

In a counterfactual world without UMP after 2008, the US would have suffered GDP losses of around 8.1% and inflation 8.8 percentage points lower by 2014Q4, while Latin American economies would have had GDP losses of around 0.5% and inflation roughly 1.5 percentage points lower — showing the high cost of not implementing these policies.

I did not find structural changes associated with the ELB in the US, UK, and Euro Area, supporting the empirical irrelevance hypothesis of the effective lower bound.

Among shadow rate estimates, Wu & Xia (2016) shows the strongest correlation with UMP measures (QE balance sheets and Forward Guidance), making it the most suitable proxy for unconventional policy stance.